Return on capital employed compares the money invested in the business (capital employed) with net (trading) profit. It shows people who have invested in the business the percentage return made with their money.

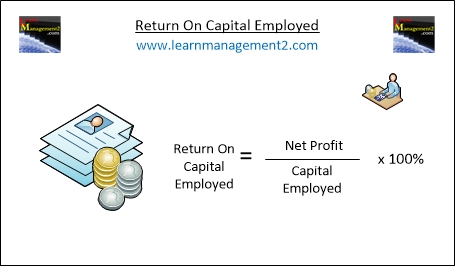

The diagram above shows how to calculate Return On Capital Employed using Net Profit and Capital Employed

What figures are used in the calculation?

Capital employed is made up of long term loans and money from the sale of shares (shareholder funds).

If you are taking figures from a balance sheet (to work out return on capital employed) use the assets employed figure if the capital employed figure is not provided. This is because on a balance sheet assets employed should equal capital employed (for more information about this click on balance sheet).

Return on Capital Employed Calculation

The following calculation is used to work out the return on capital employed

Return on Net Profit

Capital = _________ x 100%

Employed

Capital Employed

Return On Capital Employed Example Calculation

Let's imagine our firm

Made £4000 net (operating) profit

Invested £60000 shareholder funds in the firm and

Borrowed £40000 through long term loans

In our example the net profit is £4000 and the total amount of money invested in the business is £100,000 (£60,000 + £40,000).

The following calculation would be used to work out the percentage return on the money we have put into the business.

Return on £4000

Capital = _________ x 100%

Employed

£100 000

In our example the return on capital employed is 4% or to put it another way for every £100 put into the business, the business makes £4.

Conclusion

Investors in a business like to see a good return for their money so the higher the percentage figure (for return on capital employed) the better. If the figure is low investors may take their money out of the business, to invest somewhere else.

We hope you enjoyed learning how to calculate Return On Capital Employed. Here are some related articles to help you continue learning about profitability ratios